With Markets Going Down Check Your Fiduciary Liability Coverage

ERISA Imposes Liability on Employers

Be aware of loss exposures under the Employee Retirement Income Security Act (ERISA). Suits by beneficiaries can arise from drops in value of 401k plans.

ERISA applies to any program maintained by an employer for providing benefits to employees. These include retirement programs such as 401k.

WHO IS A FIDUCIARY?

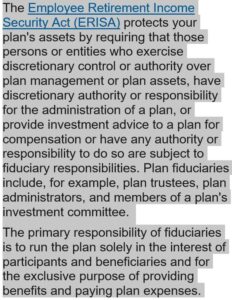

The fiduciaries of the plan are its sponsoring employer, the plan trustees, the plan administrator, all members of any plan administrative committee, the investment manager, all members of any investment committee, and anyone else who also has discretion or control over any aspect of the plan or its assets.

Fiduciaries judged to have breached ERISA responsibility are personally liable for any plan losses resulting from the breach.

From the DOL

What are the Fiduciary Duties?

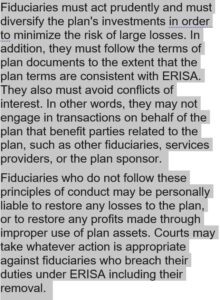

Fiduciaries must discharge their duties:

- Solely in the interest of the plan’s participants and beneficiaries;

- For the exclusive purpose of providing benefits to plan participants and beneficiaries;

- “With the care, skill, prudence and diligence under the circumstances then prevailing that a prudent person acting in a like capacity and familiar with such matters would use…”

- Diversifying the plan’s investments to minimize the risk of large losses unless it is “clearly prudent not to do so.”

- Discharging their duties in accordance with valid plan documents.

When employees are allowed to make their own investment decisions from an array of options, the employer must still be careful to provide the right mix and quality of options and to provide a certain level of information and education to employees.

You should hire an Investment Advisor who will agree to be specifically designated as a beneficiary to work with employees on their investment planning. This will help to insulate you from liability.

Fiduciary Liability Insurance

Most sizeable employers and many smaller ones carry fiduciary liability insurance which protects fiduciaries against liability arising out of breach of ERISA obligations, including defense costs. The coverage cost is very reasonable so it would be foolish not to carry it.

Setting the right limits is more art than science, but it is tied to the amount of assets in the plan. The policy limits must be high enough to cover both judgments and defense costs since both help to exhaust the limits. Also some courts have awarded attorney fees to winning plaintiffs. The reasonable premiums make it easy to have higher limits.

The largest companies have entire risk management departments reporting to the CFO. You need risk management too.

(c ) Licata Risk & Insurance Advisors, Inc. 2022

Frank Licata

mailto:[email protected]; 617.718.5901

Jun 30, 2022