The Biggest Risk Your Company Faces – CONFLICT OF INTEREST

If you’re in business, risk is everywhere. It comes from operations, from employment, from contracts, from cyber — just look around.

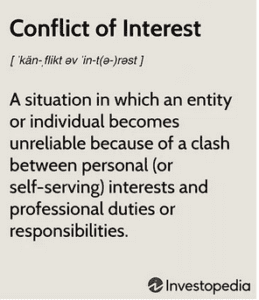

But the worst one of all is conflict of interest.

We need to know, and not deceive ourselves about, the incentives driving the people we deal with.

When we sign a business contract, say for the purchase of a commercial building, we know each side has their own objectives which might conflict with ours, so we go into it with complete awareness. Even our own lender’s needs are not totally aligned with ours. There’s no confusion here; we understand the conflict.

But one domain that is rife with conflict of interest manages to hide that fact in a fog of advertising and promotional media. That is the domain of the insurance industry.

The insurers

Are you really in good hands? An insurance policy is a contract, and the purchase of an insurance policy is a contract negotiation. We are lulled into complacency from insurer advertising telling us they are “on our side.” Of course, really they are on their own side!

See this from a prominent insurer-side lawyer at big firm White and Williams as he advises insurance company policy-writers on how they (the insurers!) can protect themselves from the horribly dangerous construction environment *:

-

“Options exist for insurers to significantly reduce their exposure for the risks associated with construction projects.”

-

“Notwithstanding that bodily injury is an ever-present risk for insureds that have construction operations, some insurers have written endorsements that can eliminate much of that exposure.”

3. “The other lesson from Lett (a court case) is that underwriters looking at construction risks can consider the nature of the insured’s operations and limit coverage as they see fit.”

* Coverage Opinions, November 1, 2012, by Randy Maniloff

Please notice he is discussing reducing the insurer’s risk by restricting policy language. Every time the insurer reduces their risk this way, they are increasing the risk of the policyholder. Construction is just one example for this discussion; the point is universal and applies to insurance for all industries.

An insurance policy is a contract, and a policy purchase is a contract negotiation!

The Brokers

How to get the real story about a broker’s role and responsibilities in their dealings with clients? From broker E&O (Errors & Omissions) lawsuits. In these suits, actions and motivations are laid bare and become public, and legal obligations are explained. Is the sales material offering “risk management” less that it appears? You decide from these nuggets:

Case 1- Baldwin Crane Equipment Corp. v. Riley & Rielly Ins. Agency, Inc., 44 Mass. App. Ct.29,31-32 (1997).

From defendant’s opposition to plaintiff’s motion: “Moreover, like other insurance agents and brokers, the defendants did not owe East Coast a duty to ensure that it understood the full import or meaning of the terms of the coverage provided.”

Case 2- Sewell v. Great Northern Insurance Co. (No. 07-1255 [10th Cir. 07/31/2008]).

The decision came down in favor of the defendant insurance broker who failed to advise a client to purchase what the insured later found to be a necessary coverage.

In explaining the decision, Atty Barry Zalma, an insurance industry columnist, stated:

“In Colorado, insurance agents have a duty to act with reasonable care toward their insureds, but, absent a special relationship …, that agent has no affirmative duty to advise or warn his or her of provisions contained in an insurance policy.”

Case 3 – Massachusetts Attorney General v. Employers Reinsurance Corp.

In a press release by AM Best, an insurer rating agency, the settlement was summarized as follows:

“The attorney general said the insurer violated the state’s consumer protection statute when it accepted a broker’s invitation to raise the price of Boston Water’s insurance after learning that Employers Re would not face competition on the account.”

See Why You Need a Risk Manager

This case is in our Broker section because it is Boston Water & Sewer’s broker’s conflict of interest we are highlighting, favoring the insurer over the client while increasing their own commission.

The attorney general of New York state has been very active in probing insurance broker activities and there are many smoking- gun emails available on this subject. We’re happy to send the cases on request.

If you’re in business, you have risk. The risk can destroy your company, or at best it can destroy your financial statement. Think of the irony of adding the risk of conflict of interest to your “risk management” efforts. Hire professionals who are completely and passionately on your team.

The largest companies have entire risk management departments reporting to the CFO. You need risk management too.

(c ) Licata Risk & Insurance Advisors, Inc. 2022

Frank Licata

mailto:[email protected]; 617.718.5901

Nov 16, 2022

Receive a free copy of this report

Please enter your contact information and we will email you a copy of this report at no charge.